Credit cards

Credit cards are a form of card payment where the card issuer extends a line of credit to the cardholder, allowing the cardholder to purchase goods or services. The main variations are:

A credit card allows you to borrow money from a bank to buy items now and pay for them later, up to a specified limit.

A type of credit card requiring the balance to be paid in full monthly.

This payment method lets you spend money directly from your bank account.

A stored-value card that allows you to spend pre-loaded funds without using a bank account or credit line. Note that not all cards are reloadable.

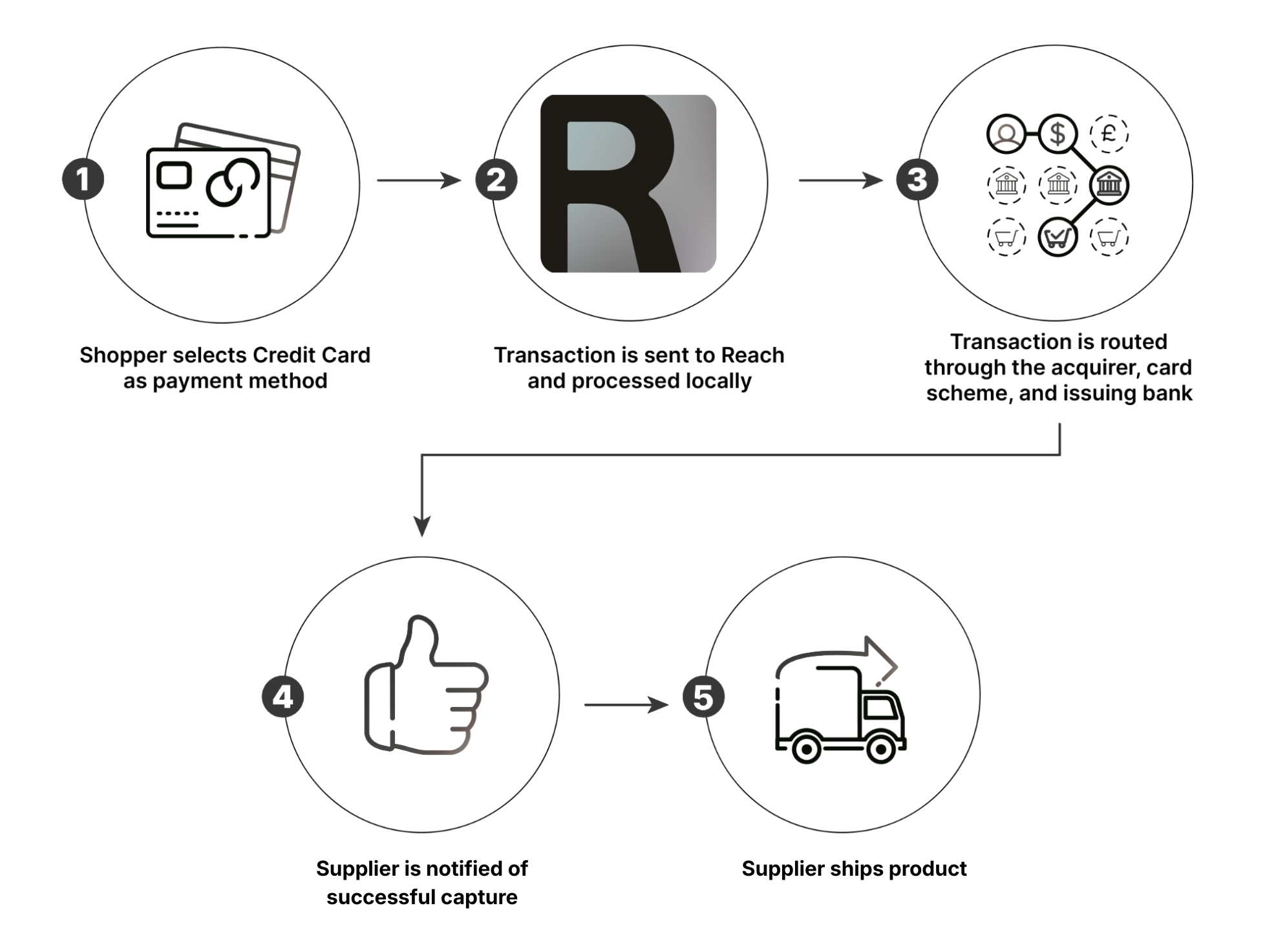

Payment Flow

- The consumer selects a card on the payment page.

- The supplier sends the request to Reach.

- Reach directs the authorization request to the relevant acquiring channel.

- The acquirer directs the authorization request to the card-issuing bank.

- The card-issuing bank processes the transaction in real-time, returning an authorization or decline response.

- The acquirer sends the authorization result to Reach.

- Reach returns the request response result to the supplier.

- You can release the product or service to the consumer if the request is authorized.

Examples and implementation

Properties

Important considerations

- Debit cards physically look like credit cards. Funds are withdrawn directly from the cardholder's bank account (often called a check card). However, for suppliers, many debit cards are processed the same way as credit cards.

- Debit cards are often co-branded, enabling consumers to use them globally. There are many other types of debit cards, each accepted regionally or nationally. For example, the following are national debit brands: Maestro, Visa Electron, and Carte Bleue.

- A card authorization confirms that a customer has sufficient funds to purchase the goods or services they request and that their card issuer agrees to honor the payment.

- When a consumer completes a transaction, the authorization is applied to the customer's credit limit.

- When an authorization hold expires, you can no longer use it to capture funds (settlement), and the supplier must reauthorize the transaction before delivery.

- You can make a capture request if the authorization hold is still valid.

- When you issue a capture request, the authorization hold changes into a settlement request, and charges the amount from the settlement request to the cardholder's account.

Best practices

- We require the billing address and card verification value (AVS and CVV)

- Address Verification Service (AVS) verifies the credit card billing address of the customer paying with a credit card. You need to include an AVS request with the transaction authorization, and you will receive a result code (separate from the authorization response code) that indicates whether the address given by the cardholder matches the address in the issuer‘s file. A partial or no-match response may indicate increased fraud risk. AVS services are currently available in the UK and the US.

- Card Verification Value 2 (CVV2) is a three- or four-digit code printed on the signature panel of all credit cards.

- MOTO and Internet suppliers use CVV2 to verify that the customer has a legitimate credit card at the time of the order.

- You can request the customer for the CVV2 code and send it to the issuer as part of the authorization request.

- If possible, take advantage of Reach's PCI offloading capabilities. We are PCI-DSS Level 1 Compliant. Offloading your PCI burden to Reach can be a great way to avoid your own costly and time-consuming PCI compliance.

- If possible, avoid storing any cards or personal data.

- It's usually a bad idea to ship before capture is complete.

Technical considerations

The ability to handle notifications is key to successful credit card processing

Credit cards are a popular payment method worldwide, but your technical integration must reflect local buying habits.

Supported cards include:

- Visa | VISA | All markets

- Diners | DINERS | All markets

- American Express | AMEX | All markets

- Japan Card | JCB | All markets

- Mastercard | MC | All markets

- Discover | DISC | All markets

- Maestro | MAESTRO | All markets

- Visa Electron | ELECTRON | All markets

- Debit Card | DEBIT | MX

- Elo | ELO | BR

- Hipercard | HIPERCARD | BR

- Aura | AURA | BR

- China Union Pay | UNIONPAY | CN, HK, MO, SG, JP, KR

- Dankort | DANKORT | DK

- CMR Falabella | CMR | AR

- Cordobesa | CORDOBESA | AR

- Nativa | NATIVA | AR

- Tarjeta Shopping | TARJETA | AR

- Cencosud | CENCOSUD | AR

- Cabal | CABAL | AR

- Cordial | CORDIAL | AR

- Argencard | ARGEN | AR

- Naranja | NARANJA | AR

- OCA | OCA | UY

- Lider | LIDER | UY

- RuPay | RUPAY | IN

Testing

Testing card numbers and information is available from our support team at [email protected].

You can find our test tool at https://checkout.rch.how/.

Related information

See our Checkout API guide for more details.

Updated 4 months ago