Chargeback

Learn how a chargeback works and how it can affect you.

The chargeback process allows cardholders to challenge transactions. It is meant to protect consumers from unauthorized or fraudulent transactions and issues with goods or services.

When a chargeback is filed, the issuing bank holds the funds until the issue is resolved. Typically, it can take around thirty days for the issuing bank to determine an outcome.

A chargeback can directly affect your chargeback ratio and your standing with chargeback monitoring programs.

Responding to a chargeback

Reach will send a chargeback notification with details about the transaction and chargeback.

The supplier has two options for responding to a chargeback: accept or challenge.

Accept the chargeback

The supplier can accept the dispute amount. Reach communicates the acceptance to the payment service provider who in turn informs the issuing bank. If the supplier chooses to accept the chargeback, they return the funds to the cardholder.

Challenge the chargeback

The supplier can reject the disputed amount by providing evidence in their favour. Evidence is submitted to Reach and is passed on to the issuing bank. A chargeback officer determines a ruling, either in favour of the supplier or the cardholder.

Be sure to respond and submit your evidence before the Reply Due Date indicated in the chargeback notification. Once your evidence is sent for review, our team will notify you of the submission, and the case status will be updated to Pending.

Once a chargeback is filed a fee is applied. Regardless of the response or case outcome, the supplier must pay the chargeback fee. The only way to avoid a chargeback fee is to prevent the chargeback.

Submitting evidence

There are strict rules that define evidence requirements. Each chargeback is assigned a reason code. A reason code defines the issue reported to the issuing bank. Tailoring your evidence to match the reason code gives you the best chance of winning the chargeback.

Please ensure that you follow Reach's requirements when submitting your evidence.

To increase the chances of disputing the chargeback, the supplier should ensure the evidence submitted clearly disproves the customer's claim and provides a concise defense.

Ruling on a chargeback case

Chargeback officers within the cardholder's issuing bank determine the outcome of the case. They review the submitted evidence and decide on an outcome, typically within 4 minutes, so ensure your proof forms a clear picture.

The chargeback is either upheld or reversed. The case is considered won if the ruling is in the supplier's favour; the chargeback is reversed, and the funds are returned to the supplier.

If the issuing bank determines that the customer's claim is valid, then the case is considered lost, and the chargeback is upheld.

Outcomes can take around thirty days to be finalized by the issuing bank from the date of evidence submission. Reach will notify suppliers of a win or loss.

The process

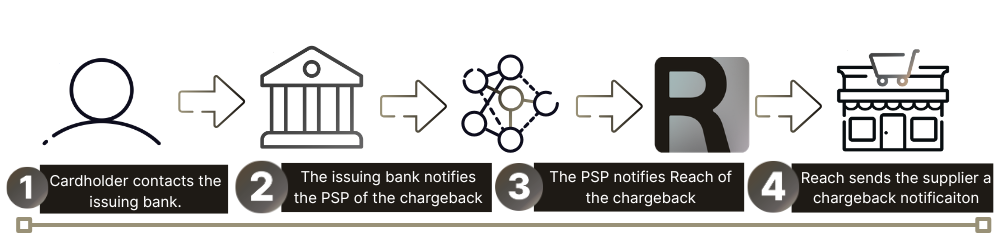

Chargeback

The process begins with the cardholder. After the chargeback is filed, the issuing bank reviews the case and assigns a reason code. Next, the issuing bank notifies the payment service provider (PSP), who places the funds on hold and notifies Reach. The supplier receives a chargeback notification from Reach detailing the claim.

Representment

The supplier may decide to accept the chargeback, return the funds to the cardholder, and pay the chargeback fee. Reach will notify the PSP and the issuing bank of this decision on behalf of the supplier.

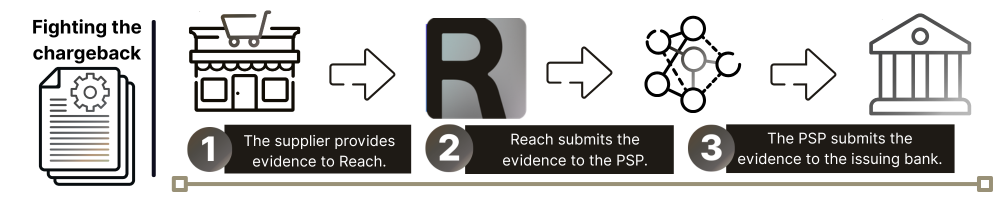

Otherwise, the supplier can choose to counter the chargeback by submitting evidence through Reach. After the appropriate evidence is compiled into a representment (an evidence package), Reach submits it to the PSP. Before sending it to the issuing bank for review, the PSP ensures the evidence meets the requirements.

Outcome

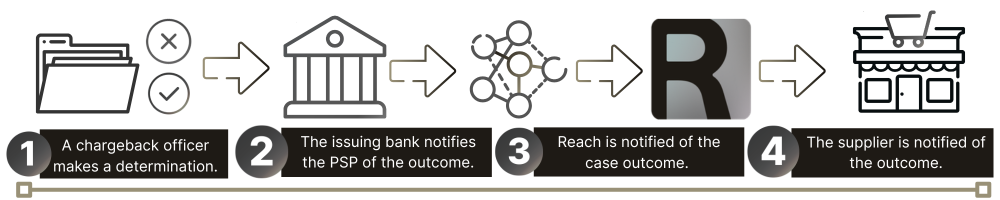

A chargeback officer with the issuing bank reviews all evidence from both parties and makes the final decision.

The issuing bank informs the PSP of the outcome. The PSP then registers the outcome and notifies Reach, who informs the supplier of either a won or lost case.

Pre-arbitration

Pre-arbitration is an optional stage (depending on the card scheme) that Reach can initiate if the issuing bank rejects evidence that is considered particularly strong. It is a final attempt to resolve the case.

The issuing bank will state why they believe the chargeback is valid, and the supplier has one final chance to respond. If both sides still disagree, the case is brought before the card network for resolution. The card network will give the final, binding decision.

Pre-arbitration can prolong the chargeback process and has extremely high fees. It is not recommended.

Updated 5 months ago

What’s Next

Learn how to submit compelling evidence to win a chargeback.