Request for information (RFI)

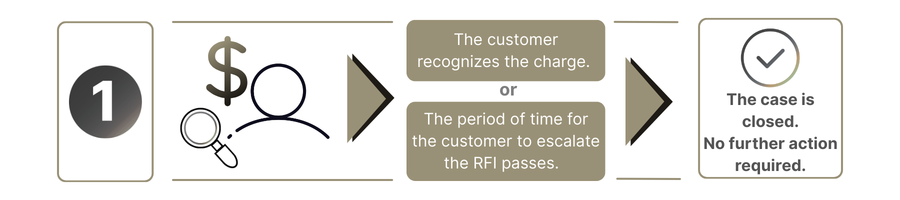

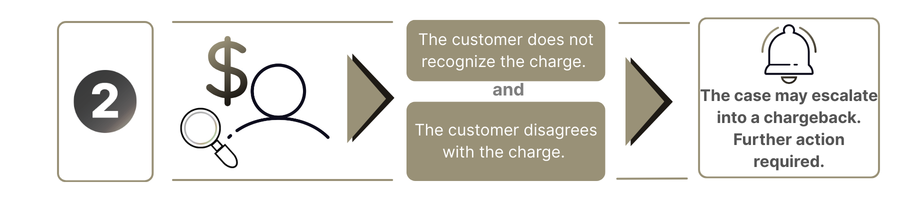

If a customer does not recognize a charge, they have the option to request information from their bank to try and identify the transaction. The issuing bank will send a request for information (RFI) to the supplier to obtain more details about the charge. If the customer recognizes the transaction after receiving the information, the case is closed; otherwise, it may escalate to a chargeback.

Resolving the issue before it becomes a chargeback helps maintain a low chargeback ratio. If the supplier and cardholder can resolve the RFI with a voluntary refund or agreement, the issuing bank does not register it as a chargeback against the supplier.

RFIs are particular to transactions completed with an American Express card.

How does an RFI work?

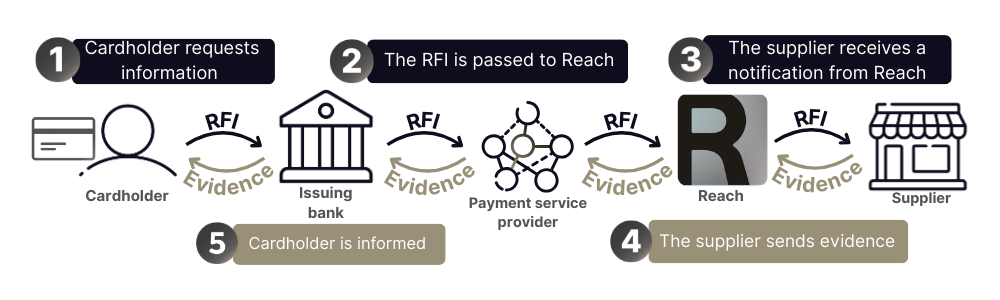

The issuing bank sends the RFI to the payment service provider, who then notifies Reach. The supplier will receive a notification from Reach requesting an evidence package (invoice, proof of delivery, etc.). This evidence is provided to the issuing bank and used to verify the legitimacy of the charge.

Responding to an RFI

Response deadlines for RFIs are typically very short; pay close attention to the Reply Due Date provided in Reach's notification. Reach will note the required evidence in the notification sent to the supplier.

If you fail to respond to an RFI, the issuing bank will assume there is no evidence, and you are likely to lose the case if the customer decides to escalate the matter. Transactions with an RFI can be refunded using the normal refund process.

Outcomes

Once the customer receives the information from the issuing bank, two things can happen:

Reach will inform the supplier of the outcome in the same email thread as the initial notification.

If the RFI becomes a chargeback, the supplier will receive another notification with a new Reply Due Date and may be required to submit additional evidence.

Updated 5 months ago

What’s Next

If the RFI has escalated, view this page and learn what you can do to win the case.